The consequences extend beyond individual data centers. On November 28, 2025, the CME Group—operator of the world’s largest derivatives exchange—experienced a complete trading halt. Treasury futures, energy markets, agricultural contracts—90 percent of global derivatives volume went dark. The cause was not a cyberattack. It was not software failure. A cooling system failed at a data center in Aurora, Illinois. The machines that price risk for the global economy exceeded their thermal limits.

The CME had sold that data center in 2016 for 130 million dollars and leased it back. When the cooling failed, CME owned nothing. It controlled nothing. It waited, like everyone else, for someone else to fix the pipes.

This single incident illuminates a truth that financial markets have not yet fully absorbed: the limit on computational throughput is not processing power. It is heat rejection capacity. The engine of global price discovery was built on silicon that melts.

IMF Chief Economist Pierre-Olivier Gourinchas drew the critical distinction in October 2025: “This is not financed by debt, and that means if there is a market correction… it doesn’t necessarily transmit to the broader financial system.” The channel through which technology bubbles become systemic crises—excessive leverage amplifying losses—is largely absent from the hyperscaler balance sheets.

Oh, yeah, these wealthy companies will totally keep the losses contained to their own cash-flows, they’re definitely not gonna try and force the public to foot the bill.

The bull case has merit. Enterprise ROI is measurable. Hyperscaler balance sheets are strong. Investment as a share of GDP remains below historical peaks. Efficiency gains may outpace demand growth.

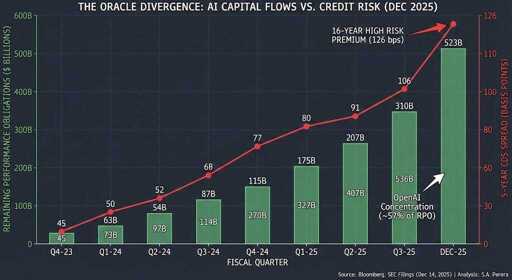

The bear case has merit. Circular financing amplifies correlation risk. Thermodynamic limits are non-negotiable. Depreciation accounting may be masking massive losses. Valuation metrics are historically extreme.

What cannot be done is to pretend that one case is obviously correct and the other obviously wrong. The uncertainty is genuine. The stakes are enormous. And the resolution will unfold not in earnings calls or analyst reports but in the quiet hum of cooling systems that either work or fail, in grids that either hold or collapse, in a physical world that operates by laws no financial innovation can repeal.

[…]

In the end, this story is not about artificial intelligence. It is about the collision between human ambition and physical reality. We have built machines that think by making machines that heat.

Machines that think. Really.

This otherwise good analysis seems to be predicated on critically digging into everything - the hardware, the financial instruments, the historical parallels. Everything except the software itself. Those claims are taken at face value.

The bull case has merit. Enterprise ROI is measurable. Hyperscaler balance sheets are strong. Investment as a share of GDP remains below historical peaks. Efficiency gains may outpace demand growth.

The bear case has merit. Circular financing amplifies correlation risk. Thermodynamic limits are non-negotiable. Depreciation accounting may be masking massive losses. Valuation metrics are historically extreme.

I like how the bull case is literally all made up vague nonsense, whereas the bear case is mostly hard facts and incontrovertible realities.

Sam Altman has already said he expects a government bailout.

Removed by mod

Machines that think. Really.

This otherwise good analysis seems to be predicated on critically digging into everything - the hardware, the financial instruments, the historical parallels. Everything except the software itself. Those claims are taken at face value.

I like how the bull case is literally all made up vague nonsense, whereas the bear case is mostly hard facts and incontrovertible realities.

This is my ‘cellar door’

Cellar door?

It’s a saying to mean a phrase or set of words that sounds pleasant due, mostly, to the combination of sounds.

(The meaning of the sentence being pleasant, too, is a bonus)

J.R.R. Tolkien, iirc, said it was the most pleasant sounding phrase in the English language.