The bull case has merit. Enterprise ROI is measurable. Hyperscaler balance sheets are strong. Investment as a share of GDP remains below historical peaks. Efficiency gains may outpace demand growth.

The bear case has merit. Circular financing amplifies correlation risk. Thermodynamic limits are non-negotiable. Depreciation accounting may be masking massive losses. Valuation metrics are historically extreme.

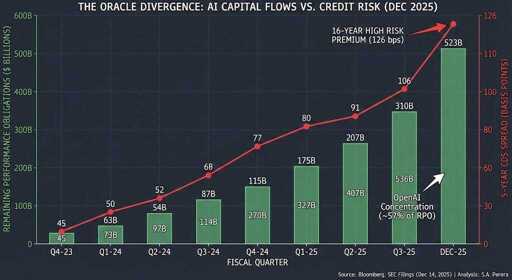

I like how the bull case is literally all made up vague nonsense, whereas the bear case is mostly hard facts and incontrovertible realities.

I like how the bull case is literally all made up vague nonsense, whereas the bear case is mostly hard facts and incontrovertible realities.